Reclusive Millionaire’s Final Warning:

Digital Lockdown Is Coming

for Your Bank Account —

BEFORE the Election

Take these three steps to protect yourself NOW:

Hello, my name is Martin Weiss

You may not know me yet … but you may know of my company, Weiss Ratings.

I founded it in 1971. Since then, it has become one of the most reliable independent financial ratings firms in America … helping regular investors avoid hundreds of financial disasters.

We correctly predicted the bank failures of the 1980s …

The Dot-Com Bust of the early 2000s …

And the Great Financial Crisis of 2008.

Those who heeded our warnings could have kept their money safe and even made substantial profits during each crisis …

In fact, The Wall Street Journal reported that our work was ranked #1 in profit performance for investors …

Beating Deutsche Bank … Merrill Lynch … JPMorgan Chase … Goldman Sachs … Standard and Poor’s … and every single other firm reviewed.

But that’s not why I’m here today …

I only mention our experience and success in predicting major financial disasters …

Because I believe a new crisis is coming to America …

And all my research tells me the first phase of this crisis will strike …

Before this November …

If the events unfold as I predict, the ultimate outcome will be so shocking …

That I just can’t stay silent in good conscience.

As an American, I feel it’s my duty to warn you about what I see coming … and show you how to protect your money before it’s too late.

The media keeps silent about this crisis. I know of no one on Wall Street that’s talking about it. And inside the Beltway, they don’t dare mention it.

But it’s a great menace lurking in the shadows — something that, when unleashed in full force, could destroy the very foundation of this country.

And I have no doubt it’s going to start happening before the coming election.

Unfortunately, most people will be taken by surprise …

If you’re not prepared, the chances are high it will be devastating to your financial future.

Millions of Americans could see their savings wiped out, their lives destroyed …

Recently, I’ve personally been spending a lot of time on a farm our family has in Southern Brazil. But with time running short, I’ve decided to fly back to the U.S. …

To record this urgent message for you now.

Because I’m not just talking about a stock market crash … I’m not just talking about hundreds of insolvent banks … or a new debt crisis …

What I’m talking about today is something much bigger and longer lasting.

And I’m going to go out on a limb to record this message for you.

So, make sure you listen till the end — and learn how to prepare …

Massive Crisis Coming Before November

Because I believe a massive crisis will begin to hit America before the November election.

And if history is any guide, it’s going to come with a chilling new wave of government overreach.

I'm talking about a sudden surge in government surveillance and interference in your private life, especially your personal finances.

It’s already possible right now, even as I record this message.

U.S. Government agencies already have the tools at their fingertips — two powerful technologies that give them far more visibility into your personal finances than anything they’ve ever had before.

One of these powerful technologies is well-known, but Americans underestimate how it can be used against them or how it could impact their money.

The other technology is so obscure that very few Americans know it exists, and even most insiders don’t understand its true power.

I’ll reveal both of these technologies in the next few minutes and I’ll show you how the government could use these tools to bring your bank account under their control.

In the next few minutes, I’m going to tell you exactly how it’s going to play out — and what to do to prepare yourself …

Including the three steps I’d urge you to take — RIGHT NOW.

I’m sure some people may discard this as a wild conspiracy … and many people may think this can’t possibly happen in America …

Well, I don’t blame them.

Conspiracy theories are commonplace today. Some have a solid basis. Many do not.

But what I’m going to tell you about today is not theory. It’s fact.

And to make sure you have all the facts, I will give you access to all the evidence, including some of the nation’s most respected research think tanks, and even top-secret documents leaked from government agencies.

Then, once you have all the facts, I’ll leave it up to you to decide what to do. You can either go about your daily life as usual, oblivious to the real dangers.

Or you can begin to take the protective action that I recommend.

But once you get close to the election, it could be too late.

The election is a critical pivot point because, as I said, the government already has the technologies it needs to invade your financial privacy and even control your financial life like never before.

What’s more, it’s hard to imagine a scenario in which the election results will not be challenged. No matter who wins!

Hard to believe? I should think not.

The crazy events of 2019 and 2020 give you the hard evidence. And the events of 2024 are already crazier.

I want to be perfectly frank with you. I am scared. I think it would be irrational not to be scared.

Right here on my desk, I have a stack of recently released studies from the government and from the nation’s big research think tanks, packed with evidence of near and present dangers.

The U.S. State Department. The CIA. The Government Accountability Office. Heritage Foundation. Gartner Group. RAND. ACLU. Kato Institute … Just to name a few.

The big question is not what or where the pressure points will be …

Not which particular crisis will be the trigger event, but …

How our government will react to those events.

For some clues, let’s check out what the people in government want and need most of all in times of crisis.

Well, they WANT control.

They want to control the people — not just people known to be causing trouble, not just people suspected of possibly causing trouble, but …

All the people, everyone, including you and me.

And they NEED money.

They need money not just to finance the bulging deficit, not just to bail out failing banks, but they also need …

Money to finance hyperactive courts …

Money to finance police forces armed to the teeth …

And money to feed their own corruption.

Until just a few years ago, it wasn’t nearly as bad.

Sure, the U.S. Treasury was running big budget deficits.

And yes, we had a growing list of banks that were at risk of failure.

But back then, the most I worried about were things I had already experienced before in the United States.

Inflation. Surging interest rates. A stock market crash. A recession. Even a wave of bank failures.

What’s more, I was able to forecast nearly all of those events with accuracy.

I was even able to name nearly all the financial institutions that failed before they failed.

Were those events bad news? You bet they were! But nothing like what I see coming now.

This is far, far worse.

Now the threat is not just the dark side of an economic crisis …

Not just the natural consequences of weak balance sheets.

Now it’s far beyond just economics and finance.

Now I’m afraid you could lose more than just your money.

You could lose your privacy, your freedom and, God forbid, your country as we know it today.

Nobody can say for sure how it will all end. But I do know some things.

I know exactly what tools the government has right now to invade our privacy.

I know exactly how the government can take away our freedom.

I’ve got hard evidence of how they’ve done it before.

And I’m going to tell you what I know right now. Not based on theory or speculation. Based strictly on the facts and hard data.

Look at what President Bush and President Obama did.

Bush started it in response to the 9-11 terrorist attacks. And in 2013, Obama expanded it long after the terrorist threat was mostly behind us.

It was run by the National Security Agency (the NSA).

The NSA illegally collected the phone records of millions of American citizens.

Not just once, but for more than five years going.

They spied on millions of people who were never suspected of any wrongdoing whatsoever.

That’s not all. The NSA and the FBI colluded with America’s biggest tech companies to spy on nearly everything you do online.

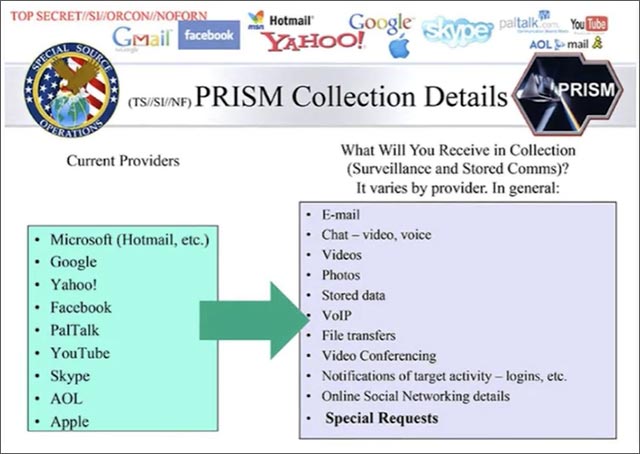

It’s all revealed in this slide from a leaked top-secret PowerPoint presentation used by the NSA and the FBI to train their agents.

Look at the left column. These are the so-called “providers,” the companies that provided your private data to the government …

Microsoft, Google, Yahoo!, Facebook, YouTube, Skype, AOL, Apple and others.

And see this list in the right column? These are your private activities that the government agents could search and spy on at any time, whether live or recorded.

Your chats …

Videos …

Photos …

Stored data …

Any file you’ve ever sent …

All the websites you visited …

Plus, details about your friends too.

What you see here was under the Obama administration, and most people think it was shut down, that our private life is not being spied upon anymore.

You wish.

Six years ago, the ACLU warned us that the U.S. government — the NSA in particular — continues to violate Americans’ internet privacy rights.

And, on April 20, 2024, President Joe Biden signed a de-facto extension of this PRISM program, Section 702 of the Foreign Surveillance Act, which is now used not only to spy on foreigners, but also on Americans.

Well, that’s bad enough. What’s worse is that a major expansion of this program could happen under any government of any political party.

All they need is an excuse to declare a “national emergency.”

A terrorist attack. A surge in the drug trade. Inflation out of control.

And what’s even scarier is the fact that the government now has far more powerful kinds of technologies ready to deploy at any time.

The first kind of technology is all over the news: Artificial intelligence. But guess who were the earliest and most prolific adopters of artificial intelligence. It was the security specialists at the NSA, the same people who were caught red-handed snooping illegally into the private lives of millions of Americans.

How do we know they’re using AI? Because they’ve “proudly” said so themselves.

The second kind of technology is not in the news.

And it’s different in a couple of ways.

You see, the government’s PRISM program was the brainchild of the NSA in close cooperation with the nation’s big tech companies. I just told you about that.

The government’s new program I’m going to tell you about now is run by the U.S. FEDERAL RESERVE with the full participation of the nation’s BIG BANKS.

And this time they have the power to do it far more directly and efficiently than they did before — by tracking all of your MONEY.

All your money in your bank account, plus …

All the money transactions to and from your bank account.

So, let’s take a peek into the future. What do we see? Well, the first thing I see is flashbacks — flashbacks to the worst and most widespread lockdown episode of our lifetime.

The lockdowns during the Covid 19 pandemic.

Over 200 million Americans barred from public transportation … and unable to visit their loved ones at the hospital …

At least 230 million Americans fully vaccinated, a large percentage of which very reluctantly or against their free will.

Even if you agreed to take the experimental vaccines …

Even if you agreed that they had to take emergency measures …

It still was like Orwell’s 1984.

It still stands as a real-life glimpse into the vast powers our government has.

It’s still a sneak preview of how the government could deploy those kinds of powers in an emergency, whether that emergency is real or contrived.

Never forget, before Covid, people thought a blanket government lockdown could never happen in America.

But it did.

And it raised a question that no one in Washington wants to answer:

If our leaders could enforce Draconian rules on American citizens during a health crisis, what’s to prevent them from doing it again in any other kind of crisis?

What will our leaders in Washington do when people can’t pay their bills?

Or what will they do when the government ITSELF can’t pay its bills …

When there’s bedlam in the streets …

When our national borders continue to melt down …

Or when an even greater emergency bursts onto the scene?

I have strong reason to believe it will all start with the one thing the government is most desperate to control: Our money.

Imagine a lockdown that’s as big — and traumatic — as we saw during the Covid crisis.

Only this time it’s not your healthcare or your whereabouts that are under government control …

This time it’s your bank account and your transactions that are under government control …

With one critical difference …

You see, unlike the pandemic, when nearly the whole country was under lockdown at the same time …

What I see coming in America — starting before November — will be far less visible … and potentially far more dystopian.

You probably won’t even know when your bank account is under surveillance …

And you may not even find out if it’s locked down …

Until the very moment you need access to your money.

Just imagine this scenario:

You log in online and all of your transactions are frozen …

You see your money is still there, but you can’t withdraw anything — all actions are grayed out.

You might shrug it off, thinking it’s a bug in your bank’s system…

So you walk to the nearest ATM.

But when you swipe your card for the third time … all you get is a blinking message saying, “transaction denied” …

You realize something else is going on …

You call your bank …

And after waiting for what it feels like an eternity, you finally get to speak to a real person …

But they can’t help you. Your account has been flagged and put under lockdown until further notice.

The reason? No idea …

“Oh. You should expect an official letter from your bank soon,” they say.

But what do you do NOW?

Your electricity bill is coming up in a few days … your mortgage is due next week … and your medical bills are long overdue …

But you have no access to your hard-earned money.

The government has taken control of it.

All of it …

Because you’re not just locked out of your checking account …

Your savings account, your brokerage account, your credit cards, your IRA and 401(k) — everything is under lockdown …

And for no apparent reason.

The Greatest Danger

Americans Have Ever Faced

You think this can’t happen to you?

Think again …

In fact, the power to do all of the above is already in place.

And it has a name: FedNow.

It’s run by the U.S. Federal Reserve with nearly full participation of America’s largest banks coming very soon.

The Fed will never admit it, of course.

But any software engineer can tell you that FedNow gives the government the technology to flip a switch and begin to control nearly every transaction in every bank account in America, probably including yours.

I’m talking about the power to freeze individual bank accounts for virtually any reason, even just based on the way you live your life.

For example, if they don’t like what you’re eating …

If they’re suspicious of a charity or political cause you donated to …

They could easily gain the power to freeze your bank account and shut down your ability to use it.

It’s actually already happened — in North America of all places …

In 2022, the Canadian government froze over 200 bank accounts of regular citizens …

Their crime?

Peacefully protesting the Covid lockdowns.

But the government wouldn’t allow any dissent …

The government labeled the protesters the equivalent of “terrorists.”

The government cut access to their money … and threw them in jail.

Even today, some of those protesters are still awaiting trial.

But that’s not all …

It was reported that people who merely donated to the cause had their bank accounts frozen, too.

Some of them were regular Americans like you …

And speaking of America …

Just a short while ago, other lockdowns have been reported.

For example, Stripe, a popular payment processing firm, locked down the account of a small business owner …

Effectively bringing her day-to-day operations to a halt …

Reportedly because she expressed the “wrong” opinion on social media.

Meanwhile, I read that a doctor from Florida had his bank account closed …

Because his views on the Covid vaccine went against the official narrative.

But the bank didn’t freeze just his accounts …

They went on to lock down the accounts of his employees too …

And these are just a few examples …

If it’s the first time you’ve heard about them … it’s because they almost never make it to the front-page news …

The government is very content to let average Americans like you and me stay in the dark, unaware of what’s happening.

In the past two years alone …

JPMorgan Chase, Bank of America, Capital One, Fidelity … to name a few …

Have locked down hundreds of accounts of groups and individuals they labeled as “promoting hate.”

But there’s no transparency, no clear definition of what that really means … and no standard process for triggering a government response.

Straight from Orwell’s 1984? Not quite. But getting closer by the day.

And what really bothers me is not simply the violations of privacy and freedom we already see today …

It’s the fact that all of this could be just a sneak preview of what’s to come.

I’ve seen it happen so many times before — all over the world — that I’ve lost count.

And now I see the growing risk that it could happen in the United States, too.

Including an unprecedented response from our federal government …

Potentially impacting millions of bank accounts in America …

Including yours … your family’s … your friends’ and your neighbors’.

How do I see it coming so vividly?

Modern Day Nostradamus

Because for the past 50 years …

My team and I have been accurately predicting nearly all major financial disasters — before they happened.

I correctly predicted the bank failures of the 1980s and 1990s …

I sounded the alarm on the Dot-Com Bust of the early 2000s months ahead of time …

People who followed my advice had the chance to get out of the stock market in time … avoid the pain … and even make handsome profits along the way …

During and since the Great Financial Crisis of 2008, I’ve named nearly all the banks that failed — or required a government bailout — with 97.4% accuracy …

Months before they failed.

On Dec. 3, 2007, I issued an alert on a major Wall Street firm. I wrote …

“Bear Stearns has sunk its balance sheet even deeper into the hole, with $20.2 billion in dead assets, or 155 percent of its equity, and it is threatened with insolvency.”

33 days later, Bear Stearns collapsed.

I also warned about Lehman Brothers well in advance, writing:

“Lehman Brothers has an even larger $34.7 billion pile-up of dead assets, or 160 percent of its equity.”

Again, I was right. Lehman went down 182 days later …

But that’s not all …

I pounded the table about Washington Mutual, Bank of America, Citigroup … and every other major bank that collapsed in 2008 — months in advance …

Today, I have a new warning …

The most important warning of my career.

Only this time, it’s not about the stock market … it’s not about inflation … it’s not about recession …

It’s about your financial freedom.

Because all the signs show that the way we live in America right now is about to change, possibly forever …

And that it’s going to start happening before the election.

It is not my intent to scare you …

God knows, we already have enough fear in America today.

But the writing is on the wall.

Former Congressman Ron Paul recently warned about what’s coming himself …

He said:

“I think we’re reaching this point where some sudden [crisis] is going to happen. I believe in that theory of the Black Swan. Yes, it’s going to pop up, and it’s not going to be controllable … it’s very very dangerous.”

— Ron Paul, former Texas Representative

I agree.

In fact, I’ve compiled a laundry list of crises that could explode with far-reaching consequences.

And any one of these could quickly turn into a major Black Swan event.

We could face a new 9/11-type terrorist attack …

Or a cyberattack that cripples our power grid, communication systems and even the federal government itself.

According to this report by the Heritage Foundation, cyberattacks by hackers sponsored and directed by nation states are probably the biggest threat to America today.

Or just look at what happened recently in Baltimore …

In Los Angeles …

In Ohio …

And never forget what’s happening at our nation’s broken borders. It’s a national security crisis on an unprecedented scale.

We could have a new pandemic …

We could have violent protests and riots in major cities across America.

The World Health Organization together with the United Nations have already started negotiations on a new pandemic treaty …

Which will legally bind all 194 member countries … including the U.S … to a unified, global pandemic control …

The U.S. dollar has lost 20% of its value since 2020 …

The U.S. government is sitting on $34 trillion in debt …

And it keeps piling on more debt at a faster and faster clip … $1 trillion every 100 days …

Things are so far out of control, some folks in Congress are now warning that that only an economic catastrophe will bring our politicians to their senses.

“I have come to the conclusion that an economic catastrophe must happen before a majority of my colleagues will get serious about curbing out of control government spending.”

— Thomas Massie

Not to mention, the Mortgage Bankers Association reports there’s $929 billion in commercial real estate debt coming due this year …

Which could lead to hundreds of banks going bust on their own.

According to Bloomberg:

“… the impact on markets and the economy will be tumultuous.”

— Bloomberg

Any one of these issues could blow up before November.

And all it would take is one crisis to give the government a pretext to switch on the sinister tools it has at its disposal.

You probably know this quote: “Never let a good crisis go to waste.”

And many people attribute this quote to Winston Churchill.

But here’s what you might not know …

The actual statement I’m referring to was issued by President Obama’s then-chief of staff, Rahm Emanuel, in response to the 2008 financial crisis.

Here’s what he said, in full:

“You never want a serious crisis to go to waste. And what I mean by that [is] it’s an opportunity to do things that you think you could not do before.”

— Rahm Emanuel, Former Chief of Staff

Take a moment to let that sink in.

He’s telling you that a crisis is an opportunity …

For the government …

To do things Americans would never accept in normal times.

And the way they do it?

They use a crisis to declare a national emergency.

Like they did back in 1933, during the Great Depression.

After Franklin D. Roosevelt was elected, he promptly declared a national emergency and issued Executive Order 6102 …

Which made gold ownership illegal for all Americans and punishable by up to ten years in prison.

Similarly, in 1971, when the U.S. government’s gold stockpiles were draining too fast …

President Nixon went on TV, declared a national emergency and took the U.S. dollar off the “Gold Standard.”

It happened again after the 9/11 terrorist attacks, with the Patriot Act allowing the mass spying on regular Americans I told you about earlier.

And more recently, in the 2020 Covid crisis …

When the government used the national emergency to crack down on your freedom of movement …

In fact, since the National Emergency Act was signed into law by President Gerald Ford in 1976 …

Our government has declared emergencies — and expanded its powers — more than 70 times

And now, we have every reason to believe they’re about to do it again …

But this time, they have all the tools they need to come for your money.

FedNow: The Devil Is in The Details

No historian in his right mind could possibly deny it.

The federal and local governments have been trying to control the way we spend our money for decades …

And always with the excuse that it’s “for your own good.”

Look what happened when governments tried to change people’s smoking habits.

They piled on a tax after tax on cigarette sales.

Did people quit smoking?

No. They started buying cigarettes from rogue vendors in the back alleys …

Visa and other major credit card companies like Mastercard and Discover even announced plans to track gun store sales …

All in the name of “safety”.

They know that when they can control the way you spend your money, they can effectively control the way you lead your life.

And this is where the government’s FedNow program comes into play.

I mentioned it earlier …

But very few people know about it, let alone understand the kind of power it gives to our federal government.

It quietly launched last year, in July 2023 …

And since then, about 470 financial institutions have already joined and many more will soon be joining the program, including:

BNY Mellon

CBB Bank

Capital One Financial …

Fidelity Securities …

First Bank …

Founders Bank

Goldman Sachs …

JP Morgan Chase …

U.S. Bank …

Wells Fargo …

To name just a few.

And keep in mind, these banks are merely part of the first phase of the rollout.

I expect this program to soon include virtually all U.S. banks, credit unions, and savings and loans.

Your bank is either already participating …

Or may be very soon.

These are the facts about FedNow, the new money system rolling out across the country even as we speak.

Now, you may be thinking:

Hey Martin, why are you so worried about FedNow …? Isn’t it just an upgrade to how banks move money?

I agree that, on the surface FedNow looks just like an overdue upgrade to our banking system …

And yes, our officials are certainly marketing it that way …

“[FedNow] will help make everyday payments faster and more convenient”

— Jerome Powell, Federal Reserve Chair

But do you believe them? Do you believe that’s all it is?

I’ve spent nearly 20 years living in Latin America and Asia. I’ve seen how apparently innocent-sounding initiatives can lead to disastrous consequences.

I can tell you flatly that, in the hands of a corrupt government, these “tech upgrades” can be transformed into control mechanisms so quickly, it would make your head spin.

I never thought this kind of control mechanism would come to America.

But it has …

Disguised as FedNow.

You see, what these officials are not telling you is …

FedNow is not just about making your transactions faster and more secure …

It’s also about surveillance …

And it’s about centralized control over your money.

At its core, FedNow is a “centralized ledger” …

It’s a system that monitors every single transaction 24/7 - practically the moment it happens …

From one … central … location.

Think about that …

What our government has been trying to do for centuries through regulations, laws and taxes …

To control the way we live our lives …

Now, can be done much more “efficiently” with FedNow.

And the way this program is designed …

You cannot “opt out.”

You won’t be able to simply switch banks.

You don’t get to vote against it.

Unfortunately, very few people outside — or even inside — the Federal Reserve understand what’s really possible.

So, let me show you how it all works …

And then I’ll walk you through the three steps I feel you must take right now - to protect yourself and your family’s savings - before it’s too late.

Central Bank Digital Control

I’m sure you’ve purchased many items and paid for many services by writing a check or swiping your card.

Or perhaps you’ve used something like Apple Pay … Venmo … or CashApp.

You’ve also made deposits in your checking account or even had paychecks set up for direct deposit automatically.

How, exactly, does the money move between your bank account and someone else’s?

It’s something we hardly think about … and yet over $2 trillion worth of these transactions happen every day.

That includes the money transactions you make … that your family makes … that your friends make … and even every company you pay or that pays you.

Not to mention Social Security payments from the government.

And it’s big. Over two trillion dollars changing hands every single day.

Most of these transactions are handled by a company called The Clearing House, which is owned by major banks.

And while the system is far from perfect, The Clearing House has been handling interbank transactions for 170 years.

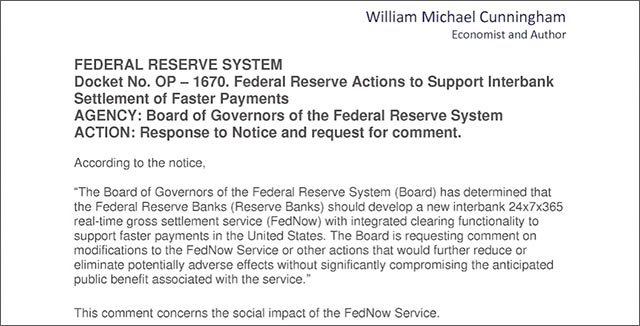

However, the Federal Reserve saw the chance to make it “better.” And in 2019, with little fanfare or press coverage, they released a document named Docket No. OP-1670.

Not many people have heard about it, let alone read it …

But they should have …

Because this document describes in great detail how a “centralized ledger” … like the one used by FedNow … could improve and replace what The Clearing House has been doing for over a century and a half.

It’s all here, in black and white …

It even reveals how to centralize all transactions handled by private payment systems, such as Apple Pay, CashPay, Google Pay, PayPal, Venmo, Zelle and many more.

Like I said, about 470 institutions have already enrolled just since FedNow was launched last year …

With some banks joining as we speak.

The bad news is most people have no idea what’s happening …

And yet, the Federal Reserve is on its way to becoming the central war room in charge of all payment systems, with the power to monitor and even control how you spend and receive money.

They have their hands on the entire process.

For example …

You’re probably aware that banks already require you to fill out special IRS forms if you attempt to withdraw about $10,000 or more in cash.

Well, with FedNow, merely transferring money from one place to another - in practically any amount - could raise a red flag.

And not only that …

With FedNow, the government could instantly know what you are buying, in what amount, and from whom …

Did you fill your gas tank one time too many this month?

Did you buy meat or dairy from a local farmer who’s not “certified”?

Did you donate to the “wrong” candidate?

All of that - and more - could instantly raise flags and lock you out of your money.

This is about controlling your lifestyle …

Social credit scores …

Digital IDs …

Vaccine passports …

A gateway to digital tyranny.

And it all starts with FedNow.

To be fair, I see a lot of people also warning against a Central Bank Digital Currency - or CBDC …

U.S. Senators Ted Cruz and Rick Scott have even introduced a bill to ban it …

But the truth is, all of that is just a distraction …

The government doesn’t need a CBDC to take control of your money and your life …

They could easily do it with FedNow. The surveillance and centralized control are already here …

Soon, I predict nearly every single financial institution in America will become a part of it.

And so will your bank account … your brokerage account … your credit cards … your IRA and 401(k) … your mortgage … your Apple Pay, PayPal or Venmo.

Once your money is in the system, the government will have instant access to it.

If you find this hard to believe, just remember what our government has already done.

Never forget: In 2013, the National Security Agency spied on millions of American citizens.

And this time, the spying I’m talking about won’t be run by the NSA. It will be run by the Federal Reserve.

You cannot stop it …

But you still have time to protect your financial future … by taking the three steps I’m going to show you in just a moment …

FedNow is just the start …

Because if you think that spying on you … controlling your life … and shutting you out of your money for “dissident behavior” is the only risk you face …

I think you’ll soon find out you’re mistaken.

Another big nightmare will be taxes.

Just imagine, with FedNow …

Every dollar that comes in and goes out of your account could be subject to taxation.

That $400 you got from selling your old sofa on eBay.

Or the $135 your friend sent you over Venmo for his share of the restaurant bill.

It could soon be on you to prove to the government that it’s not income …

And you will have to fight to get your money back.

Look, they already plan to hire 87,000 new IRS agents to go after hard-working Americans …

There’s nearly $80 billion in new funds allocated just for that.

But FedNow is far cheaper.

FedNow could allow them to monitor everything that comes into your bank account and tax you right then and there, as it happens …

Without costing them a single penny beyond computer programming time.

Worse, thanks to the latest developments in Artificial Intelligence, they may not have to spend hardly any money on computer programmers.

It could be mostly executed automatically by a highly specialized AI algorithm.

You really think the government is not going to abuse that?

They used the Great Depression to confiscate gold …

They used the recession of the 1970s to take the U.S. dollar off the Gold standard …

And they used the Covid pandemic to go on a money-printing spree that put us $34 trillion in debt …

Three Steps to Protect Your Money - Before November

Mark my words …

When the opportunity shows up, the U.S. government won’t think twice about coming after your money …

The Federal Reserve just reported a historic net loss of $114.3 billion … and suspended all remittance to the Treasury.

This has never happened before - it’s the first time they lost money in 108 years.

What are the odds, when the next crisis hits, that they won’t conjure up an unexpected tax on everyone’s wealth?

If history is any guide, the answer is self-evident …

It doesn’t matter what you say.

Once the U.S. government has instant access to your money, they get an enhanced power to tax you.

Let me be clear: This is not a matter of if - it’s a matter of when …

Unfortunately, most people will be caught by surprise …

By the time news is out, it will be too late.

And if you’re waiting for your preferred presidential candidate to stop all of this all of the sudden, don’t hold your breath.

Because it doesn’t matter who wins - Democrat, Republican or Independent …

They won’t be able to reverse it.

The system is already in place, ready to go.

What’s worse …

The government doesn’t even need a crisis … or a national emergency … to expand its Draconian powers.

Which means, even if we somehow get lucky … and manage to avoid the worst of the looming crisis before November …

It doesn’t change the facts.

Because thanks to FedNow, the government has quietly installed a system capable of nearly complete financial surveillance on all Americans.

And if they decide you’re not in “compliance” with whatever their policy agenda dictates at the time …

They have the technology to lock down your bank account …

And it’s very possible you won’t find out until it’s too late.

So don’t risk your financial future by waiting on the sidelines …

There is a way to avoid all of this … provided you take action while there’s still time to do so in a planned and deliberate manner, without panic or rash judgments.

And that’s why I’m here today …

I’ve found a way to protect your financial future in three simple steps, which I’m going to show you right now …

In fact, my team and I have been helping regular Americans protect their retirement nest egg … and grow their wealth … for over five decades …

And now, I’m going to share this knowledge with you …

STEP #1

Move Your Money off the Grid

(But Not Off Shore)

So let me come right out of the gate and say it …

The best way to protect yourself from the government’s prying eyes …

Is to split your money up and get some of it out of the system, away from U.S. banks …

One way to do it is to buy gold.

However, you must do it the right way, which I’m going to explain in a minute …

First, there’s a new asset on the rise. I call it, Gold 2.0 …

And it’s quickly becoming one of the most important investment asset classes in human history …

I’m talking about Bitcoin.

This is my step number one: Get a portion of your money out of the system by buying some Bitcoin.

Why:

What makes FedNow so worrisome is that it’s a centralized ledger. Bitcoin is the exact opposite.

It’s decentralized. There’s no company that owns it, there’s no CEO, no decision-making committee.

Which means the government can’t send the feds to raid anybody’s headquarters and shut it down.

In fact, the blockchain, the technology behind Bitcoin, runs on tens of thousands of computer nodes all around the world. And each of these nodes has their internet addresses protected by multiple layers of encryption.

To even attempt to stop Bitcoin would be an impossible task. The government would first have to shut down the entire internet - and keep it that way forever …

Even then, Bitcoin doesn’t need the internet to exist. It can also be transferred over radio signals, satellites, local area networks and much more …

But what if the government decides to ban it … like they banned gold back in 1933?

I’m 100% certain they won’t do that for two reasons:

There are no safes with pallets of Bitcoin. It’s not a tangible asset like silver or gold. It’s ultra-secure computer code. It’s locked up forever, and no central organization or government has the keys.

The only way to get your coins is by using a secret 24-word passphrase, which serves as an encryption key.

If you can memorize this phrase or you can keep it in a safe place, you can store unlimited amounts of Bitcoin off the grid.

And second, it’s already too late for any government to ban Bitcoin in their own country, let alone globally. The genie is out of the bottle …

According to Newsweek, over 46 million Americans already own Bitcoin. And NBC reports that 1 in 5 Americans has invested, traded or used cryptocurrencies. That’s 20% of all adults in the United States …

Many of them are rich, well-connected elites … and even politicians themselves …

If the government even hints at a ban …

The backlash would be so big that no politician supporting the ban could ever win an election again.

That’s why the smartest billionaire investors in the world like Elon Musk … Mark Cuban … Kevin O`Leary … Jack Dorsey … and Michael Novogratz … just to name a few …

Have all invested a portion of their wealth in Bitcoin.

Even Warren Buffett … a long-time Bitcoin critic … has now profited massively himself from investments in the crypto sector.

And so should you …

Not only is Bitcoin a great way to move your money away from the government’s prying eyes …

But it’s also one of the best ways to grow your nest egg with relative speed.

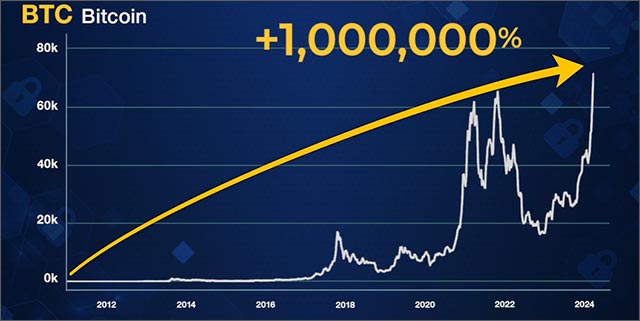

Since Bitcoin began trading, it’s up by over one million percent …

And as I mentioned earlier, the U.S. dollar lost 20% of its value in four years, since 2020 …

But get this: Bitcoin went up 1,154% during the same amount of time …

Think about it …

If investors had put $1,000 in the bank at the beginning of 2020, they could have the equivalent of $800 right now.

In contrast …

If they had bought $1,000 worth of Bitcoin - they could be sitting on $12,000 right now.

Not to mention, just in the last six months, Bitcoin has surged another 174% …

Even Larry Fink, the CEO of the biggest asset management firm in the world, BlackRock … has had a change of heart on Bitcoin …

Back in 2017, he famously claimed that Bitcoin is “an index of money laundering” …

But just a few months ago, he reversed his opinion, announcing that, “Bitcoin could revolutionize finance …”

And then he filed for permission to launch his own Bitcoin ETF.

What happened next? Well, on January 10, the Securities and Exchange Commission (SEC) approved 11 spot Bitcoin ETFs.

The ETFs started trading on the very next day …

And in the days that followed, Bitcoin’s price jumped by over 50%.

But that is just the beginning …

The arrival of ETFs — Bitcoin ETFs — means that a lot more people will rush into Bitcoin … pushing its price far higher.

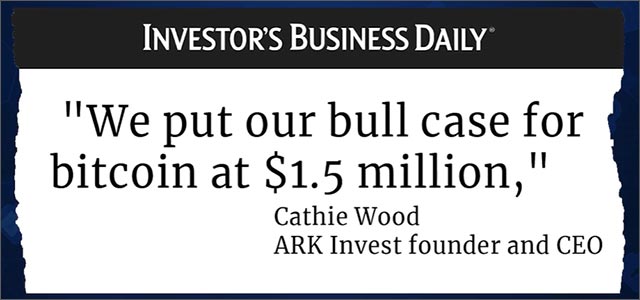

Analysts at the research firm Bernstein expect Bitcoin to reach $150,000 by next year …

And Cathie Wood, the famed money manager and CEO of ARK Investments, recently said the price of a single Bitcoin could hit $1.5 million by 2030.

That’s another 2,182% increase in just five short years.

Adding to the upward price momentum, this is the year of the Bitcoin halving, which has now cut new Bitcoin supplies in half.

You don’t have to be an Ivy League economist to understand what happens when demand grows (from ETFs) … and supply shrinks (from the halving).

If history is any guide, I expect Bitcoin price to continue rising at a rapidly accelerating pace until the end of 2025.

So if you don’t own Bitcoin yet, now is the right time to get in - before the election - while you still can.

I’m not suggesting you sell the farm …

But as you can see, if you don’t allocate at least some portion of your assets to Bitcoin - you could be losing money …

While remaining vulnerable to the government’s prying eyes and even control.

We will show you, step by step, what we believe is the single best way to buy Bitcoin, and then safely move it away to get your money off the grid.

But here’s the thing …

Historically, every time Bitcoin has gone up, the price of most smaller cryptos have moved up even faster.

Like we saw recently when select coins brought back returns of:

2,001% …

5,400% …

Even 10,200% or more.

I believe once-in-a-lifetime crypto gains are still in front of us …

And we’ve identified a handful of little-known coins we believe that average investors should own right now, together with Bitcoin.

These are all projects working on improving our current financial system …

Making it decentralized and harder for the government to seize total control.

Right now, you can still get in for a tiny fraction of Bitcoin’s price, but I don’t expect that to be the case for long …

I’ll share all of the details about these unique projects with you in my special briefing called “Digital Lockdown: How to Protect Your Money From Government’s Control”.

I will also show you, step by step, how to buy them - along with Bitcoin - and then store them away from the government’s reach.

We’ll share details how to get this report in just a moment …

But while buying digital assets like Bitcoin and similar cryptos could be great … This Step #1 is not enough.

You need to also take Step Number Two …

STEP #2

Buy Gold the Right Way

I mentioned earlier it’s always a good idea to have some portion of your cash in physical gold …

This is an asset I’ve been pounding the table about for almost four decades …

And for good reason. Throughout history, we’ve seen paper money lose its value, even become next to worthless, while gold has a 5,000-year track record maintaining or growing it’s value.

Unfortunately, most people buy gold the wrong way …

If you want to keep your gold safe, without the risk of it being confiscated or frozen …

You’ve got to learn the secret to buying and storing gold the right way. The same way many of the ultra-wealthy do it.

That’s why, I want to send you this second bonus report called “The Ultimate Gold War Chest”.

In this report, I reveal:

- How to get the best deals in gold …

- How to buy gold the right way and avoid the scams many investors fall for …

- How to store gold correctly so your wealth is protected in any scenario …

- How to avoid losing your gold by spotting all the sneaky tricks used by thieves …

- How to prevent your gold from ever be confiscated again by implementing this little-known “Gold Confiscation Loophole” …

And so much more!

On top of that, we will reveal how, in an environment similar to today’s, investors have used gold to grow their wealth by 5x or more …

Simply by buying gold at the right time.

You know, since our top gold analyst began recommending gold, it’s done just that — it’s up by more than 5.5x its value …

And there’s a system to do that most people don’t know about …

I’ll share details on how to get this bonus report, together with the bonus report “Digital Lockdown: How to Protect Your Money From Government’s Control” at the end of this video …

And that leads me to Step Number Three …

STEP #3

Move Investments Off Wall Street

Now, I must warn you. This new step might not be for everyone …

So, if I were you, I’d make sure to move ahead with at least the first two steps as soon as possible …

Before the next crisis hits and it’s already too late.

However, if you decide to keep some - or most - of your money in the stock market, on Wall Street …

Well, your financial future could be in greater danger than most Americans realize.

In contrast, the types of investments I’m recommending in Step Three …

Will keep you away from traditional brokers … away from exchanges … banks … and other institutions that may soon be swallowed up under FedNow …

While at the same time, they will keep you protected from inflation, bank failures, recession or worse.

This is the secret that ultra-wealthy elites don’t want you to know …

But it’s one of the reasons why many of today’s hedge fund titans, venture capitalists, banking elites and royal families …

Are not only able to preserve their massive wealth - but grow it even further …

And in nearly all market conditions!

For example, over the years, one of these alternative investments has surged 2,341% …

Another one appreciated 22,627% …

And a third of these off-the-grid investments has skyrocketed a staggering 447,268% …

How is this possible?

Simply because these “secret” investments have one unique quality …

When the economy is in shambles …

Be it recession or inflation, stock market crash or bond market collapse …

These investments rarely go down.

Case in point …

2022 was one of the worst years in the last decade …

The U.S. bond market was down 13% …

The S&P 500 fell 20% …

The Dow Jones Industrials dropped over 25% …

Even Bitcoin fell sharply.

All of these asset categories, including one of the most conservative (bonds), delivered painful losses.

In contrast, the off-Wall Street investments I’m talking about now went up by 29% - on average - during the same period.

As you can see, this is a great way to get your money away from banks, away from Fed control …

And if I’m just halfway right about how this crisis is going to unfold, it’s also a great opportunity to watch your money grow and compound, especially if you can wait for the passage of time to work its magic.

We reveal everything you need to know about these little-known investments … and how to get started … in our third bonus report called “How To Protect And Grow Your Wealth Off Wall Street” …

When you’re armed with all this valuable information, together with your other two bonus reports, “Digital Lockdown: How to Protect Your Money From Government’s Control” and “The Ultimate Gold War Chest” …

You can be well on your way to protect your - and your family’s - financial future, starting today.

Here’s How to Get Started

Now, I want to be clear …

The amount of research that goes into these kinds of reports is extensive.

That’s why, I normally restrict access to this information to our paid subscribers only …

But these are unprecedented times.

The way we live our lives in America is about to change drastically …

And I want to do everything in my power to help you protect yourself and your family from what’s coming.

So it’s critical that you start taking these three steps now - while you still can …

Before the election …

And before it’s too late.

That’s why I want to make this decision a no-brainer for you …

And rush these three reports to you right away.

The only favor I ask in return is to try our risk-free membership service Safe Money Report, or Safe Money for short.

The vital information you’ve learned today, is the kind of intelligence my team and I have been gathering for years …

And it’s available to our Safe Money members every month …

We warn you about threats to your savings and retirement that are right around the corner …

So you’re always one step ahead of everyone else.

You’ll also get regular updates of our Safe Money model portfolio, so you’ll know exactly when to get in on an investment and how much to allocate …

And when we see the opportunity to take out some profits, we’ll send you an alert.

Rest assured, no matter what happens, my team at Safe Money will help you navigate every step of the way …

Like when we helped our members avoid hundreds of bank failures …

Or when we warned our subscribers about the tech stock meltdown …

And those who listened to our advice could have avoided the bloodbath and a drop in their portfolios of as much as 75% …

Or when we warned them before the collapse of Bear Stearns … Lehman Brothers … Washington Mutual … Citigroup … Wachovia … and many others …

People who listened to our advice could have kept every single penny of their retirement savings and investments … while others risked losing practically everything.

When you join Safe Money today ….

You have the chance to get the same kind of foresight and expertise working to protect and grow your retirement …

For over 40 years, Safe Money has published lists of the most vulnerable banks and stocks BEFORE a crisis sent them plummeting.

Not only that, we’ve also published lists of companies that are the most likely to THRIVE despite any chaos.

We’ve built a track record that has gotten the attention of Barron’s … Forbes … Fortune magazine … The New York Times … and The Wall Street Journal.

They have all recognized our ability to identify the losers and the winners … and to predict market events.

Barron’s wrote that Weiss is “The leader in identifying vulnerable companies.”

The New York Times wrote “Weiss was first to see the dangers and say so unambiguously.”

We have built a massive database on more than 53,000 companies and investments … with the world’s only rating system that’s 100% independent.

Our team of analysts, mathematicians and data scientists use this system to cut through all the noise and detect early warning signals.

This is how we were able to accurately predict the bank failures of the 1980s … the dot-com collapses of the early 2000s … and the Great Financial Crisis of 2008

As a member of Safe Money, you get access to all of that - and more …

Here’s Everything You Get …

When you join Safe Money today, you get …

Our complete solution designed to protect your money and grow your wealth outside the government’s control. That includes immediate access to your three bonus reports:

- Bonus report #1: Digital Lockdown: How to Protect Your Money From Government’s Control (sold separately for $79)

- Bonus report #2: The Ultimate Gold War Chest (sold separately for $79)

- Bonus report #3: How To Protect And Grow Your Wealth Off Wall Street (also sold separately for $79)

You’ll get a full year of our monthly Safe Money Report (normally soldfor $129) with our model portfolio based on our prize-winning ratings …

Plus you get:

- 24/7 premium access to all 53,000 of our Weiss ratings. That includes nearly every bank, credit union, insurance company, stock, ETF and mutual fund in America (previously sold for $228 per year).

And you also get our …

- Weiss Ratings Daily. Our members-only news alerts delivered to your inbox every morning (priceless).

All told, that’s a value of $594.

But you won’t have to pay nearly that much.

We’re living in unprecedented times. There’s no time to waste …

Waiting on the sidelines could cost you dearly.

That’s why I’m doing everything in my power to make this decision as easy as possible for you.

Your cost for this entire package is just $49.

You save 92% and get an extra $545 in value beyond your meager cost. And you get a full year to decide if Safe Money Report is right for you.

All with my …

100% Money-Back Guarantee

That’s right. Your subscription cost is risk-free.

Download your bonus reports now. Get our Safe Money reports and investment recommendations for the next 12 months. Stay up to date with our daily alerts for the next 365 days.

Then make your decision …

If you’re not happy with everything that Safe Money can do for you, just let us know and we’ll give you a 100% refund, no questions asked.

Even if you cancel on the very last day of your subscription, you can still keep everything we’ve sent you all year long, my way of saying “thank you” for giving Safe Money a try.

I want you to feel comfortable with our research and recommendations.

Because I’m 100% convinced that once you have the chance to dig into your bonus reports and see the potential value of our service …

You’ll want to stick around with us for the long haul.

That’s why I’m confident in giving such a generous refund policy.

If this sounds like a good deal to you, then please click the button below to get started …

And don’t worry, before you sign up, I’ll give you the chance to review all the details of this offer.

But I think you’ll agree, with all the crazy and crazier things happening all around us …

The time to act is now …

The longer you wait …

The closer we get to the election …

The higher the risk to your financial future.

It’s not the time to sit passively on the sidelines.

It’s the time for action.

Right now, you have a decision to make - for yourself and for your family …

When the next crisis hits … when nearly everything we cherish is going up in flames … when others all around you are caught up in turmoil …

I trust you’ll look back on this day and be thankful you made the right decision.

So I’ll take you to my Safe Money webpage right now.

To give you the opportunity to escape government control … and grow your wealth along the way.

Good luck and God bless!

Martin D. Weiss, PhD

Weiss Ratings Founder